Being aware and prepared for whatever might come down the fraud path may be an objective for every forex trader worth his mettle, but, to be successful at this art form, keeping abreast of key Market Risk issues is also paramount to surviving the whims of foreign exchange trends. In that vein, now is a good time to step back from general fraud concerns and learn a few lessons from the quarter that has just transpired. Yes, the first quarter of 2018 is now in the history books, so to speak, and market complacency is no longer a given going forward. Volatility and global tensions have ramped up a notch, and there is no sign that calm, placid waters will be the prevailing theme in quarters to come.

The general rule in all global markets is that “Risk never sleeps.” A simple definition of Market Risk is as follows: “Market risk is the possibility of an investor experiencing losses due to factors that affect the overall performance of the financial markets in which he or she is involved. Market risk, also called “systemic risk,” cannot be eliminated through diversification, though it can be hedged against.”

The diagram above is just one of many used to describe the primary sources of market risk. The factors displayed are general in nature, but each wields its share of power when influencing market directions, whether up or down. Keeping an eye on how each is behaving or trending at the moment is paramount to understanding what fundamental forces are driving market actions, especially in the foreign exchange markets. A brief description of each source from an accredited investment service is as follows:

1) Equity Price Risk: Equity price risk is the risk that arises from security price volatility – the risk of a decline in the value of a security or a portfolio. Equity price risk can be either systematic or unsystematic risk. Unsystematic risk can be mitigated through diversification, whereas systematic cannot be. In a global economic crisis, equity price risk is systematic because it affects multiple asset classes. A portfolio can only be hedged against this risk. For example, if an investor is invested in multiple assets that represent an index, the investor can hedge against equity price risk by buying put options in the index exchange-traded fund.

2) Inflation Risk: Inflation risk, also called purchasing power risk, is the chance that the cash flows from an investment won’t be worth as much in the future because of changes in purchasing power due to inflation. Analysts also tend to include interest rate risk in this same category. Interest rate risk is the risk of increased volatility due to a change of interest rates. There are different types of risk exposures that can arise when there is a change of interest rates, such as basis risk, options risk, term structure risk and re-pricing risk. Basis risk is a component due to possible changes in spreads when interest rates are fluctuating. Basis risk arises when there are changes in the spread between different markets’ interest rates.

3) Currency Risk: Currency risk, or foreign exchange risk, is a form of risk that arises when there is volatility in currency exchange rates. Global firms may be exposed to currency risk when conducting business due to imperfect hedges. For example, suppose a U.S investor has investments in China. The realized return will be affected when exchanging the two currencies. Assume the investor has a realized 50% return on investment in China, but the Chinese Yuan depreciates 20% against the U.S. dollar. Due to the change in currencies, the investor will only have a 30% return. Currency exchange-traded funds offer ways to hedge forex risk .

4) Commodities Risk: Commodity price risk is the volatility in market price due to price fluctuation of a commodity. A commodity’s price is affected by politics, seasonal changes, technology, and current market conditions. For example, suppose there is an oversupply of crude oil, which has caused oil prices to fall every day over the past six months. A company that is heavily invested in oil drilling wells faces commodity price risk. The company’s profit margin will fall as well, since it is still operating at the same cost but the prices of crude oil are falling. Its profits will decrease. The company could use futures or options to hedge this risk and minimize the uncertainty of oil prices.

Price fluctuations in any or all of these areas can cause volatility to ramp up, as uncertainty grips the minds of investors and analysts. As every forex trader has learned, volatility can be a good thing, if and when you see it coming and can prepare for its impacts. Foreign exchange markets, however, can also have a mind of their own, as capital flows behind the scenes suddenly change direction. The other three risk areas can be taking their toll, but currency rates can react to a number of other fundamental forces, as well. Experienced traders develop an intuitive feel for which forces are taking charge and creating predictable fluctuations, the kind that offer favorable profit opportunities.

Read more forex articles.

What lessons can be learned about Market Risk from the first quarter’s action?

The initial quarter for 2018 was a bit of a roller coaster in our global financial markets. From a momentum perspective, the S&P 500 index continued its ascent, but then corrected, then rebounded, and finally corrected once more. European and Asian indices performed in a similar fashion, but decidedly more on the downside with tighter wave amplitudes. The era of sublime complacency has gone by the wayside. Volatility is back, at least enough to make trading a more interesting pastime.

What happened to cause such a departure from previous predictability? From a pure factual basis, the S&P 500 index recorded its first quarterly loss since 2015. On a daily basis, the same index rose or fell one percent or more on 23 separate occasions to the astonishment of all. European shares, however, were taking a beating during the same three-month period, depreciating some 4.5% for the quarter. At the same time, the Euro moved ever northward from 1.20 to 1.23, showing no signs of backing down. On the commodities front, Crude Oil also bounced from $60 to $65 a barrel. Is inflation beginning to rise?

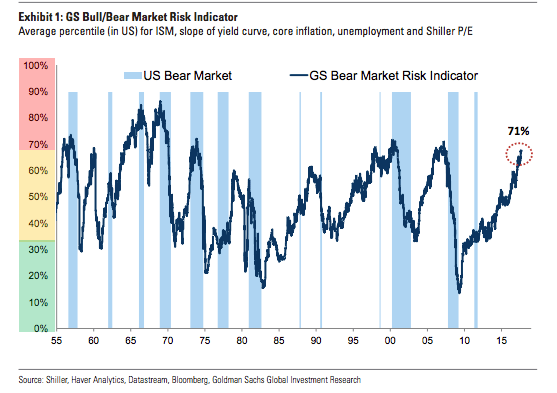

2017 may go down in history as the “Goldilocks” year, a year where inflation was not too low and not too high. The reasons given by most analysts for the sudden swings of volatility in February were due to inflation scares. It was easy to get complacent when one believed that global growth was synchronized, so to speak, as major central banks coordinated their monetary policies and painted a picture that inflation was under control and not a problem. To act otherwise would be to destabilize markets and create a mad scramble to re-allocate capital accordingly, a scenario hinted at by a recent comment by analysts over at Goldman Sachs:

“Low unemployment in the US (and other places like Japan, the UK and Germany) and strong growth momentum at such an advanced stage in the economic cycle would normally already be associated with higher wages and, consequently, higher inflation and tighter monetary policy (pushing all variables up together on their historical measures of risk). It is because of the lack of inflation that some of these variables can appear stretched without ringing alarm bells for equity investors. Put another way, it is very unlikely that without core inflation rising much, policy rates will rise sufficiently in the US or elsewhere to invert yield curves and/or force a recession in the near future.”

The bank also included the following chart to drive home its point:

It is typical at this point to remind everyone that the past is no guarantee for how the future might react, but the chart seems to imply rough times ahead. Goldman, however, is actually saying that the chart is not as bad as it looks, that inflation may not jump in a material fashion, which could then trigger an overreaction by the Fed to apply the brakes suddenly, invert the yield curve, and make a recession a near-term reality.

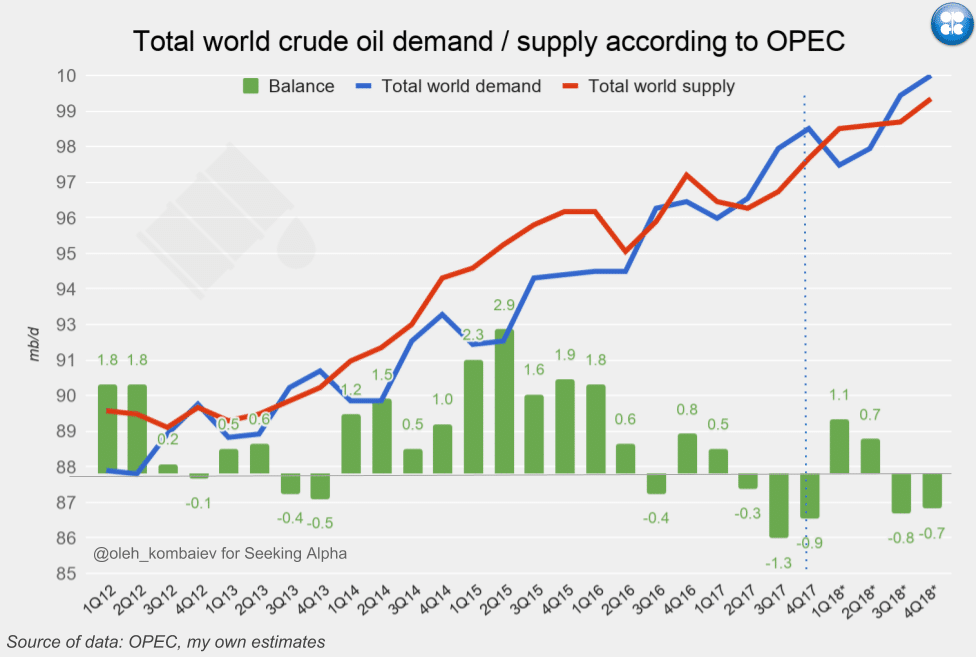

The commodity sector has been heating up, as well, if we use crude oil as a general barometer. As one analyst noted: “What is happening in the Middle East and in Oil Markets is just another piece of the story and is really becoming more and more prominent in other major markets. Since late June of last year, the Thomson Reuters/Core Commodity CRB Index has risen by 18 percent.” Other analysts have penned articles “about the rise in the producer price index and about the increases in food prices and the turnaround in gas prices and the possibilities of these going higher in the near future.”

Recent price increases in crude oil prices have been noted above, but OPEC projections seem to indicate that the so-called “supply glut” in oil is over (See below):

And then we have uncertainty surrounding trade tariffs and agreements, along with further implications of trade wars to come. Of note, “Equities are going to be on the front lines in terms of what gets hit first from ongoing geopolitical/trade war jitters. That notion was underscored two weeks ago when the tit-for-tat exchange between Washington and Beijing led directly to the worst week for U.S. stocks in more than two years. That risk-off move was accompanied by a bid for Treasurys, which gathered momentum.”

Concluding Remarks

Uncertainty and volatility are back! The first quarter of 2018 was a rocky road and may be an excellent harbinger of things to come. Market Risk elements are moving in tandem to eliminate complacency and force investors to re-evaluate their positions going forward. The primary concern for this year, as stated in poll after poll of the analyst community, is how quickly will inflation jump from the starting gate. Any press release that hints at the slightest inkling of an accelerating pace will naturally cause disruptions in our financial markets.

The days of major forex pairs treading water within tight boundary limits may finally be behind us. Market Risk components appear to be vibrating to the same tune at the same time, a rare event indeed. Our capital movement infrastructure now is also highly dependent upon technology. Machine-driven algorithms can easily over react, creating a potential liquidity-crunch scenario like never before experienced. Market volatility could skyrocket at the drop of a hat, thereby presenting huge opportunities for gain for those traders that are prepared for the action.

To be forewarned is to be forearmed!

Related Articles

- Forex vs Crypto: What’s Better For Beginner Traders?

- Three Great Technical Analysis Tools for Forex Trading

- What Does Binance Being Kicked Out of Belgium Mean for Crypto Prices?

- Crypto Traders and Coin Prices Face New Challenge as Binance Gives up its FCA Licence

- Interpol Declares Investment Scams “Serious and Imminent Threat”

- Annual UK Fraud Audit Reveals Scam Hot-Spots

Forex vs Crypto: What’s Better For Beginner Traders?

Three Great Technical Analysis Tools for Forex Trading

Safest Forex Brokers 2025

| Broker | Info | Best In | Customer Satisfaction Score | ||

|---|---|---|---|---|---|

| #1 |

|

Global Forex Broker |

BEST SPREADS

Visit broker

|

|

|

| #2 |

|

Globally regulated broker |

BEST CUSTOMER SUPPORT

Visit broker

|

|

|

| #3 |

|

Global CFD Provider |

Best Trading App

Visit broker

|

|

|

| #4 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #5 |

|

Global CFD & FX Broker (*Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more) |

ALL-INCLUSIVE TRADING PLATFORM

Visit broker

|

|

|

| #6 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #7 |

|

CFD and Cryptocurrency Broker |

CFD and Cryptocurrency

Visit broker

|

|

|

|

|

|||||

Forex Fraud Certified Brokers

Stay up to date with the latest Forex scam alerts

Sign up to receive our up-to-date broker reviews, new fraud warnings and special offers direct to your inbox