Newcomers to forex trading are frequently inundated with disclaimers on every forex website that trading currencies is high risk and that special training is a requirement to swim in these shark infested waters. For those that heed these warnings, they soon learn in their basic course of study that adhering to prudent risk management techniques and managing the size and number of open positions are paramount to success. As an accomplished trader, however, you also need to be aware of risk levels at all times.

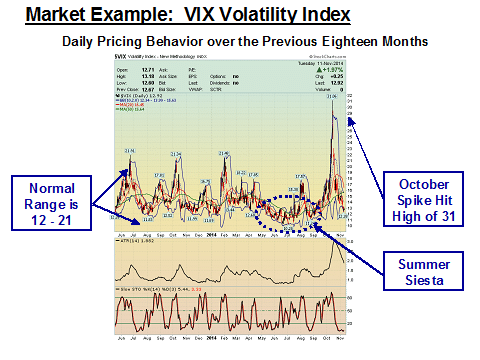

How does one assess and measure market risk levels? To begin with, risk equates to uncertainty, and when markets are uncertain, they are volatile. For the highly technical forex trader, implied volatilities for various currencies can be discerned from the futures market and can give guidance to expected trading bandwidths. One can assess the actual volatilities for individual pairs by keeping tabs on their respective Average True Range (ATR) indicators. For the general market, however, traders typically follow the behavior of the VIX volatility index. Here is a chart for the past eighteen months:

Per one website source, the “VIX is a trademarked ticker symbol for the Chicago Board Options Exchange Market Volatility Index, a popular measure of the implied volatility of S&P 500 index options. Often referred to as the fear index or the fear gauge, it represents one measure of the market’s expectation of stock market volatility over the next 30-day period.” The VIX figures are percentages that forecast with 68% probability the annual expected range of the S&P 500. To convert to a monthly range, you would divide by 3.46 (the square root of 12) or 7.21 for a weekly forecast.

Critics claim that the VIX is merely a measure provided from current index options, using complex calculations derived from the Black-Scholes equation. It is not an accurate forecast of the future thirty days out. Much of this kind of debate is academic in nature, but, as a forex trader, you are only looking for a general feel of how other traders are thinking. Are they nervous? Are they uncertain? Will volatility translate into chaos, which means more opportunity in the forex market? The VIX will give you a quick read, so to speak, accepting of course that currency pairs are highly correlated to stock markets and the S&P 500 index, another tenet taught in basic training classes.

As the chart depicts, volatility fell through the floor this past summer, as if everyone sold in May and stayed away until August and September, a summer siesta of sorts. It even appears that a quarter of the trading community got nervous mid-vacation, returned to their screens, and modified their open positions in August. The herd returned after Labor Day, assessed market conditions, and then went crazy in October, trading with reckless abandon. The winner was the U.S. Dollar, as sanity returned to the global marketplace.

The VIX has now returned to the lower boundary of its normal trading range. The tenor of the futures market is one of consolidation, almost pausing to contemplate the next major moves. The U.S. market continues to lead the global economic recovery, but Asia and Europe are both having to resort to an easing of monetary policy and other central banking tricks to boost their domestic economies into higher gears. The fear of another recession, however, hangs over Europe, and their major trading partners are holding their collective breaths.

Concerns that more volatility is ahead and that a liquidity crunch, similar to 2008-2009, is imminent are beginning to surface. Guy Debelle, an Assistant Governor of the Reserve Bank of Australia, recently shared these comments with a symposium of bankers in Sydney, “There are also some misplaced perceptions amongst market participants about the degree of liquidity present in some market segments. That strikes me as a dangerous combination and unlikely to be resolved smoothly.” Debelle knows full well that if the estimated $11 trillion in carry trades unwinds abruptly, Australia will suffer.

Charles Hugh Smith, another forex analyst of note, has gone further to posit that, “Risk cannot be disappeared, it can only be transferred or temporarily hidden from view.” This time around, he believes the beast is hiding out in foreign exchange, especially for emerging market countries. Experts have often believed that risk can be totally hedged, but the financial collapse of five years back destroyed that myth. Statistical pricing models depend on normalcy within two standard deviations, but outside of these norms, the so-called fat-tail anomalies can wreak havoc on any theory and decimate liquidity.

Smith sees many disturbing similarities in our current situation that harken back to the last financial crisis. Investors have globally chased return in our low-interest-rate environment, concentrating capital in emerging market debt denominated in Dollars. His sober warning is: “The risks unleashed by central bank funding of massive carry trades, policy-driven devaluations and currency crises have yet to manifest. When they do, we’ll rediscover why traders consider the FX market the 800-pound gorilla that stomps on the stock and bond markets without even noticing the squishing sound.”

The simple message is keep your eye on risk measures and react accordingly!

Related Articles

- Forex vs Crypto: What’s Better For Beginner Traders?

- Three Great Technical Analysis Tools for Forex Trading

- What Does Binance Being Kicked Out of Belgium Mean for Crypto Prices?

- Crypto Traders and Coin Prices Face New Challenge as Binance Gives up its FCA Licence

- Interpol Declares Investment Scams “Serious and Imminent Threat”

- Annual UK Fraud Audit Reveals Scam Hot-Spots

Forex vs Crypto: What’s Better For Beginner Traders?

Three Great Technical Analysis Tools for Forex Trading

Safest Forex Brokers 2025

| Broker | Info | Best In | Customer Satisfaction Score | ||

|---|---|---|---|---|---|

| #1 |

|

Global Forex Broker |

BEST SPREADS

Visit broker

|

|

|

| #2 |

|

Globally regulated broker |

BEST CUSTOMER SUPPORT

Visit broker

|

|

|

| #3 |

|

Global CFD Provider |

Best Trading App

Visit broker

|

|

|

| #4 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #5 |

|

Global CFD & FX Broker (*Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more) |

ALL-INCLUSIVE TRADING PLATFORM

Visit broker

|

|

|

| #6 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #7 |

|

CFD and Cryptocurrency Broker |

CFD and Cryptocurrency

Visit broker

|

|

|

|

|

|||||

Forex Fraud Certified Brokers

Stay up to date with the latest Forex scam alerts

Sign up to receive our up-to-date broker reviews, new fraud warnings and special offers direct to your inbox