When the Bee Gee’s crafted the disco song, “Stayin’ Alive”, in 1977, little did they know that this rock ballad about surviving on the streets of New York would eventually become the rallying cry of one foreign exchange broker, FXCM, as it struggled for survival on New York’s Wall Street. Success stories in the forex space have been few and far between of late, but the FXCM storyline has been emblematic of how things can go from bad to worse, even for a major player traded publicly on a stock exchange.

The beleaguered broker has been in the headlines recently, once again liquidating property after property in a last gasp attempt to raise capital. Unfortunately, the buzzards of Wall Street are circling on high, waiting to feast on the carrion below. Share prices continue to fall to new depths, resulting lately in a market capitalization below $15 million, the prerequisite standard for remaining with the big boys on the New York Stock Exchange. FXCM is not dead, at least not yet. Many of its customers have remained loyal, even after the CFTC banned it from operating on U.S. shores. How loyal, you might ask? Last quarter revenues were $49.2 million, no small sum in today’s world.

Last march, we wrote: “When the fickle finger of regulatory fate points in your direction, you had best move on and do whatever it takes to survive. FXCM went from being the largest forex broker in the United States market to being immediately excommunicated by the CFTC from the region, a story that may be stranger than fiction, but surely received everyone’s attention in our industry. Reputation risk is the issue, and when a management team plays fast and loose with this imperative, judgment can be swift and harsh as a consequence.”

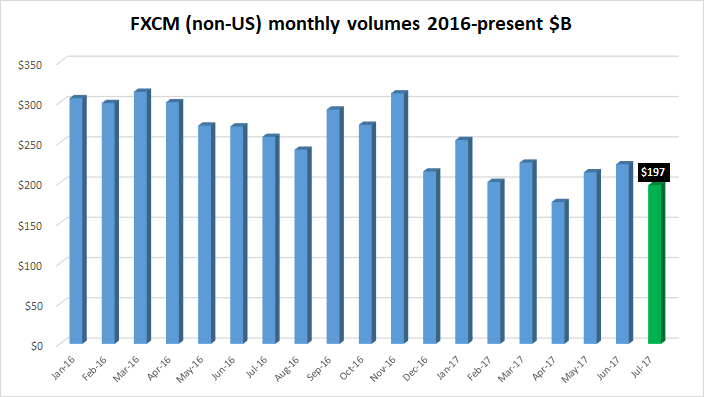

The firm maintained its New York headquarters address, but was forced to sell its domestic client base to its formidable competitor, GAIN Capital, for a measly $7 million and change. Management receded to foreign capitals and contented itself with its international customer base, which, at the time, had been estimated to constitute 82% of its business. Even as the summer slowdown paired back trading volumes for all brokers across the industry, FXCM still managed to book $197 billion in turnover in July, an impressive feat considering its crippled status.

We also wrote that, “In order to emphasize the global nature of the firm, FXCM, Inc. has re-branded its efforts going forward and will now go by the name of Global Brokerage Inc. and trade under the symbol of “GLBR”. GLBR has offices in London, Europe, and Australia and an Introducing Broker (IB) network that spans the globe, as well.” GLBR owns 51% of the Retail FXCM operating entity, and it is the shares of GLBR that fell 26% on fears that the firm’s shares will soon be de-listed from the Nasdaq.

The current “crisis”, as it is being termed in the press, is that delisting will occur if GLBR shares do not “exceed $15 million for 10 consecutive business days between now and October 30, 2017.” Unfortunately, GLBR is currently worth roughly half of the required amount. As it noted in recent quarterly filings, “The company is actively working with financial and legal advisers to explore a potential restructuring.”

Delisting would demote shares to a much smaller exchange, where liquidity would be constrained, and new capital issues would arise. A delisting event would also trigger the fall of several other dominos that presently exist in various debt contracts of the firm. In other words, major debt pay downs would require a sizable amount of cash on hand, an amount that does not exist today. As a result, FXCM, i.e., GLBR, is marketing every salable asset on its balance sheet.

Read more forex articles

How did FXCM go from market share leader in the U.S. to whipping boy?

A brief stroll down the road of FXCM’s checkered past is in order at this point. At one stage, FXCM was the market share leader in the United States market by a healthy margin. Times were good, as the happy faces in the picture below will attest:

An Internet chronicle of the firm’s early history may serve as a harbinger of questionable business practices later down the road: “Forex Capital Markets was founded in 1999 in New York, and was one of the early developers of online forex trading. In January 2003, FXCM entered into a partnership with Refco group, one of the largest US futures brokers at the time. Refco took a 35% stake in FXCM and licensed the FXCM software for use by its own clients. Refco filed for bankruptcy on October 17, 2005, a week after a $430 million fraud was discovered, and two months after its initial public offering of stock. Refco’s CEO Phillip R. Bennett was later convicted of the fraud. FXCM became entrenched in the Refco bankruptcy proceedings for several years.”

What happened down the road? FXCM grew quickly over the following decade, perhaps, due in part to a marketing ruse that was exposed by the CFTC in 2017. The prevailing retail forex business model at the time was known as the “dealing desk” or market-maker system of trading with customers. Brokers would accept the opposite side of client transactions, thereby benefiting when the customer would lose on a trade. The level of distrust raised by this arrangement continued to exacerbate, until several innovative brokers instituted a new “no dealing desk” approach. Client trades would be immediately matched with the best bid from a selection of “liquidity providers” that would then bear the risk of the trade.

FXCM was ostensibly one of these innovative firms that implemented this new way of handling customer trades, and it marketed its refined “ethical” approach to its extreme advantage. Financial headlines soon touted a new player in the big leagues: “In December 2010, FXCM went public and began trading on the NYSE, becoming the first forex broker in the U.S. to issue stock to the public.” FXCM had come a long way in a short period of time, and Drew Niv, its founder and CEO, was heralded as a miracle-maker in the foreign exchange industry.

In its IPO prospectus, FXCM expounded upon its unique trading proposition: “When our customer executes a trade on the best price quotation offered by our FX market makers, we act as a credit intermediary, or riskless principal, simultaneously entering into offsetting trades with both the customer and the FX market maker. We earn fees by adding a markup to the price provided by the FX market makers and generate our trading revenues based on the volume of transactions, not trading profits or losses.”

All was fine and good for Niv, FXCM, its clients, and its stockholders, until January 15, 2015, a day that will live in infamy in the foreign exchange industry. Swiss central banking officials suddenly, without any prior notice, lifted the Swiss Franc peg to the Euro. A shockwave immediately went through the global forex world, once that resulted in billions of dollars lost in an instant. Traders, banks, hedge funds, and brokers on the wrong side of the trade paid dearly. FXCM was hit for $225 million, but wait, how could a “no dealing desk” broker engaging in “riskless” trades lose such an enormous sum?

There had been inklings in the form of consumer complaints that something might be astray in FXCM’s back office. Class action lawsuits had been poring in, “alleging fraud and racketeering from deceptive and unfair trade practices, and misleading shareholders during the 2010 IPO.” Subsequently in 2011, the NFA and the CFTC assessed fines for slippage malpractices to the tune of $2 million and $6 million, respectively. A major loss of $225 million, however, could not be associated with minor slippage defalcations.

FXCM was now out of compliance with CFTC capital requirements. As reported, “Drew Niv, to his credit, quickly found a “White Knight” in the form of the Leucadia Capital, a hedge fund that was willing “on a handshake” to provide an emergency loan of $300 million. Leucadia, unfortunately, inherited the mess that would eventually be exposed in 2017. It, too, must now deal with angry shareholders, as well.”

What was exposed in 2017? Per the CFTC: “FXCM went so far as to write internal algorithms that routed trades to a controlled entity that shared 70% of its revenues with the firm, amounting to $77 million from 2010/2014. It also concealed its interest in the market maker and filed false statements with the NFA. FXCM, Adhout and Niv are permanently barred from NFA membership, FXCM can no longer operate in the U.S., and FXCM has agreed to pay a $7 million fine.” The firm has been reeling to this day.

What are recent headlines saying about the death throes of FXCM?

Actual headlines have been running both positive and negative, a mixed bag, so to speak. On the surface, operating results are not that bad, as depicted below:

The volume trend presented above is in line with industry averages. Forex trading volumes have been falling, but seem to have bottomed out. Operating turnover is one thing, but the health of a firm, however, resides on its balance sheet, and therein lies the problem. The firm is cash poor at the moment. Debt covenants will soon be triggered that require hundreds of millions of dollars in pure hard cash. Consequently, FXCM has been marketing every non-essential asset to interested buyers in the marketplace, but distressed sellers are rarely able to negotiate favorable sales terms.

Lawsuits are piling up, and non-U.S. regulators have yet to opine on the subject matter. The FXCM defense has always been that forex trading is pure speculation, laden with heavy risk. Drew Niv, the former chief executive of FXCM, has openly stated in the press that, “If 15% of day traders are profitable, I’d be surprised.” Losing money while trading forex is to be expected. Brokers are not the bad guys, just the enablers.

Concluding Remarks

Are we witnessing the final days of FXCM/GLBR as we know it? Will it be restructured, be acquired, or close its doors permanently in the near-term future? Pending lawsuits, regulators, and stock exchange officials seem to have its management team in a stranglehold at the moment. One “White Knight”, Leucadia, has already been burned. We doubt if another is in the wings. Yes, client bases can be sold to the highest bidder, but is there another massive fraud in the background that has yet to be exposed?

If you are a loyal FXCM customer, tread very carefully in these shark-infested waters!

Related Articles

- Forex vs Crypto: What’s Better For Beginner Traders?

- Three Great Technical Analysis Tools for Forex Trading

- What Does Binance Being Kicked Out of Belgium Mean for Crypto Prices?

- Crypto Traders and Coin Prices Face New Challenge as Binance Gives up its FCA Licence

- Interpol Declares Investment Scams “Serious and Imminent Threat”

- Annual UK Fraud Audit Reveals Scam Hot-Spots

Forex vs Crypto: What’s Better For Beginner Traders?

Three Great Technical Analysis Tools for Forex Trading

Safest Forex Brokers 2025

| Broker | Info | Best In | Customer Satisfaction Score | ||

|---|---|---|---|---|---|

| #1 |

|

Global Forex Broker |

BEST SPREADS

Visit broker

|

|

|

| #2 |

|

Globally regulated broker |

BEST CUSTOMER SUPPORT

Visit broker

|

|

|

| #3 |

|

Global CFD Provider |

Best Trading App

Visit broker

|

|

|

| #4 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #5 |

|

Global CFD & FX Broker (*Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more) |

ALL-INCLUSIVE TRADING PLATFORM

Visit broker

|

|

|

| #6 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #7 |

|

CFD and Cryptocurrency Broker |

CFD and Cryptocurrency

Visit broker

|

|

|

|

|

|||||

Forex Fraud Certified Brokers

Stay up to date with the latest Forex scam alerts

Sign up to receive our up-to-date broker reviews, new fraud warnings and special offers direct to your inbox