The largest forex broker in the U.S. market, FXCM, and its CEO, Drew Niv, have been ordered to cease doing business in the United States for misleading its clients for a period of five years, ending in 2014. FXCM is headquartered in New York and listed on NASDAQ (formerly traded on the NYSE). As of December 31, 2016, it had commanded the largest share of the domestic retail forex business, beating out its rivals with a 34% share of the market. News out today is that FXCM will sell its U.S. accounts to Gain Capital, subject to regulatory approval, which will make Gain the new domestic market leader with 58%.

A fine of $7 million was also assessed jointly upon Niv and his founding partner, William Ahdout, both principals agreeing to “withdraw from CFTC registration; never to seek to register with the CFTC; and never to act in any capacity requiring registration or exemption from registration, or act as a principal, agent, officer, or employee of any person that is registered, required to be registered, or exempted from registration with the CFTC.”

Why so stiff a penalty and verdict? Per the CFTC release, “FXCM engaged in false and misleading solicitations of FXCM’s retail foreign exchange (forex) customers by concealing its relationship with its most important market maker and by misrepresenting that its “No Dealing Desk” platform had no conflicts of interest with its customers.” FXCM went so far as to write internal algorithms that routed trades to a controlled entity that shared 70% of its revenues with the firm, amounting to $77 million from 2010/2014. It also concealed its interest in the market maker and filed false statements with the NFA.

Regulators are not happy with the current state of the retail forex trading industry and its exorbitantly high level of customer complaints that have been accelerating over the past few years. The FCA and CySEC recently did their level best to rock the industry in December by proposing new draconian guidelines that would seriously cut into present broker revenue streams and impair the ability of all brokers to attract new clients to their respective product and service offerings. It seems that it was only a matter of time before the CFTC followed suit in its jurisdiction, but this time, the focus was on a single broker.

Read more forex trading news

FXCM is no stranger to major headline news stories

Back in January 2015, FXCM was one of the major casualties of the now infamous “Swiss Franc Debacle”, when, as we had reported, “The Swiss National Bank (SNB) removed its 1.20-peg to the Euro. Many highly-leveraged positions and automated trades from robots and EAs were caught short when the maelstrom occurred last week. Many brokers halted trading until sanity returned. In some markets, a 40% swing in the “EUR/CHF” currency pair valuation was not uncommon.” Losses for FXCM were substantial, somewhere in the neighborhood of $300 million.

Bells and whistles went off at the CFTC related to capital adequacy, but to the amazement of all, FXCM quickly arranged for an emergency infusion of exactly $300 million in capital from Leucadia Capital, apparently just “on a handshake”. When the CFTC learned that the related capital was not permanent in the form of proceeds from a stock offering, but that, “The “new capital” turned out to be a high-interest 2-year loan with a “forced sale call option”, terms that almost guarantee a future liquidation at some point,” it more than likely commenced an intensive on-site audit of the brokerage.

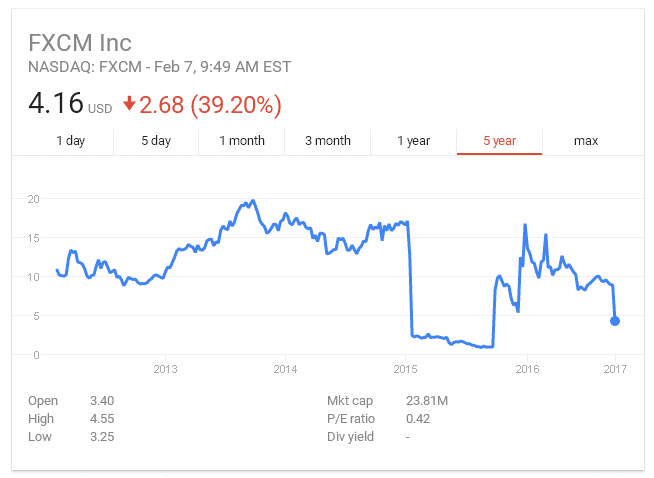

To its credit, FXCM gradually recovered from the ashes, rebuilding its stock price that had plummeted some 90% during that dark January period. As the chart below depicts, however, FXCM shareholders have bitten the cruel dust once again:

The previous fall from grace had led to a transfer from the NYSE to the NASDAQ, when share prices fell below the $1-level and remained there for an extended period of time. The firm’s CEO Drew Niv, recognized as one of the best in the industry, had been given a great deal of credit for rebuilding the brokerage “with remarkable calmness and poise”, a feat that warded off many adverse shareholder lawsuits that had been pending. FXCM is primarily a forex broker for North America, but it is global in nature. It has offices in London, Europe, and Australia, and it has an extensive Introducing-Broker network that could become problematic, as time goes by.

Oh! What a tangled web we weave when first we practice to deceive!

The limited disclosures provided by the CFTC highlight a very technical backroom web of deception that could only have been orchestrated by the two men at the helm: “FXCM, the Order finds, formulated a plan in 2009 to create an algorithmic trading system, using an FXCM computer program that could make markets to FXCM’s customers, and thereby either replace or compete with the independent market makers on FXCM’s “No Dealing Desk” platform.” FXCM spun off the routines into a separate company, but failed to disclose how closely aligned the two firms were going forward.

The facts demonstrate that trading volumes were slanted toward this entity, EFFEX Capital, and that a 70% sharing of revenues resulted. If the funds did not flow directly back to FXCM, then there may be grounds for more punitive criminal actions. As for direct harm to traders, it would be extremely difficult to determine if there had been direct gains or losses. The overall process is not that much different than how the “Dealing Desk” model operates today.

The software gamesmanship appears to be nothing more than a clever way to market to customers and Introducing Brokers that FXCM was following the new wave of STP brokers that claimed to take the ethical high road. At the time of its development, the “No-Dealing-Desk” model was gaining traction and moving share in the market. The FXCM “trick”, as it were, was to enjoy the best of both worlds, as long as no one was the wiser. Publicly traded companies must comply with a host of regulations and disclosure requirements to protect investors, but this bit of deception became lost in the paperwork, until CFTC and NFA officials stumbled upon it.

How did knowledgeable industry insiders react? One banking executive remarked, “I do not see how this is any different from any bank liquidity provision practices in this business. You always reject trades off market against the maker and fill the one against the client. Fair or not, it is not for me to judge but this is how FX has always functioned. If people want to change the rules, okay let’s do it going forward but why any authorities would fine people for accepted market practices is beyond me.”

Another opinion was more blunt: “While EFFEX had an unfair advantage versus other liquidity providers by knowing where other providers were pricing, CFTC and NFA could not nail FXCM for much on the effect of this setup on clients and this is why the fine is so small. In the end maybe some other liquidity providers did not get the flow because of EFFEX but EFFEX got the trades by showing the best price to clients.”

If traders may have benefited, then who are the damaged parties?

If there is one lesson that our court system has taught corporations, it is that disclosures of risk to the consumer must be complete, evident, and transparent. Class action attorneys have thrived on this simple notion, and judges and juries have granted damage claims in the millions for anything that even mildly approached an offense of this basic legal principle. If you are using a marketing gimmick to attract customers and then take advantage of them, be prepared to pay the Piper handsomely.

The foreign exchange industry is complex. Counterparty arrangements abound, but if there is an inkling of doubt at any point in the process, liquidity will evaporate like snow in the desert. Unfortunately for FXCM, its web of business partners had withstood an initial shock in 2015, but this time around, lawsuits may come from a variety of sources. Here is a brief recap:

- FXCM Shareholders: New lawsuits will be filed, as well as old ones being resurrected, since these actions pre-date the Swiss Franc Debacle. The evidence is compelling that the management team willingly and knowingly chose to act in a way that could destroy the firm. Gross incompetence carries with it hefty consequences;

- Network of Introducing Brokers (IBs): FXCM announced that it will be transferring its U.S. client base to Gain Capital, “subject to regulatory approval and a definitive agreement.” The accounts constitute less than 20% of the firm’s revenue base. The transfer, however, will abruptly revise all existing commission agreements to IBs in an instant. The level of distrust is already palpable, and the loss of substantial income could stimulate a separate round of litigation. More importantly, as one expert noted, “Bearing in mind that this execution model has a global presence and that customers and introducing brokers will likely never trust FXCM ever again, there is a distinct likelihood that the firm will not recover from this.”

- Leucadia Capital Shareholders: The original bailout agreement was done “on a handshake”, without the level of due diligence that would have been expected in order to risk so high a level of immediate support. As a result, Leucadia is now heavily entwined in this mess, having taken a 49.9% interest in FXCM’s operating companies. If FXCM goes down, the losses for Leucadia could be substantial. It presently has a market cap of $8.5 billion, having shed a cool $500 million in one day’s trading. Its shareholders are litigation savvy and will certainly weigh in on the latest catastrophe;

- FastMatch Divestiture: FastMatch is a business partnership that was launched in 2012 by FXCM, Credit Suisse, and BNY Mellon to do exactly the opposite of what FXCM has been found guilty of – to provide “an electronic communication network (ECN) which offers large pools of diversified liquidity with complete impartiality.” FXCM will most likely be forced to sell its 32% share in the enterprise.

Concluding Remarks

The CFTC has spoken, and the news is not good for FXCM. As one pundit opined, “We also need to see if there is a follow up from the FCA and other regulators globally as a result.” FXCM may soon become a broker without a country. Whether FXCM can survive the series of attacks to come will be a continuing saga, a story with legs, so to speak, and we are only on the very first chapter. Stay tuned!

Related Articles

- Forex vs Crypto: What’s Better For Beginner Traders?

- Three Great Technical Analysis Tools for Forex Trading

- What Does Binance Being Kicked Out of Belgium Mean for Crypto Prices?

- Crypto Traders and Coin Prices Face New Challenge as Binance Gives up its FCA Licence

- Interpol Declares Investment Scams “Serious and Imminent Threat”

- Annual UK Fraud Audit Reveals Scam Hot-Spots

Forex vs Crypto: What’s Better For Beginner Traders?

Three Great Technical Analysis Tools for Forex Trading

Safest Forex Brokers 2025

| Broker | Info | Best In | Customer Satisfaction Score | ||

|---|---|---|---|---|---|

| #1 |

|

Global Forex Broker |

BEST SPREADS

Visit broker

|

|

|

| #2 |

|

Globally regulated broker |

BEST CUSTOMER SUPPORT

Visit broker

|

|

|

| #3 |

|

Global CFD Provider |

Best Trading App

Visit broker

|

|

|

| #4 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #5 |

|

Global CFD & FX Broker (*Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more) |

ALL-INCLUSIVE TRADING PLATFORM

Visit broker

|

|

|

| #6 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #7 |

|

CFD and Cryptocurrency Broker |

CFD and Cryptocurrency

Visit broker

|

|

|

|

|

|||||

Forex Fraud Certified Brokers

Stay up to date with the latest Forex scam alerts

Sign up to receive our up-to-date broker reviews, new fraud warnings and special offers direct to your inbox