86% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Assessing the risk in the foreign exchange retail trading arena can be a difficult task at best, from following important data releases, reports about brokers and their fiscal health or lack thereof, down to analyzing technical charts of your chosen forex pairs. From time to time, it also helps to take a break and check on the activities of major infrastructure players in the industry, especially the publicly traded ones that must comply with stiff disclosure regulations that ensure transparency. Two of our favorites are Playtech and Plus500, both traded on the London Stock Exchange and both, competitors to a degree.

Three years back in 2015, Plus500 was literally on the ropes after regulators landed the boom on them, but Playtech and its precocious billionaire, Teddy Sagi, rushed in with an attempt to save the enterprise with a modest takeover bid. Mr. Sagi had previously built his Playtech over a few years into a juggernaut in the industry. He also knew a bargain when he saw one in Plus500, but regulators in both the UK and Ireland stepped in to squash the deal. By that time, Plus500 management had dealt with its regulatory issues and was ready to regain its previous momentum.

The tabloid press had a field day with this marriage-on, then marriage-off drama. In the process, we quickly learned how profitable gambling entities can be, but oversight responsibility in the UK switched over to the FCA in January of this year, and ESMA in the EU came down hard on CFDs and even harder on binary options with new regulations that went in force in July. Both firms have since shied away from the binary option space, but CFDs are still fair game. The recent travails of these two offer up a tale of two companies that even Charles Dickens would curry favor with, but far, far better days lay out in the future, if recent investments by hedge funds are good indicators.

86% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

What is going on with Playtech during its Post-Sagi days?

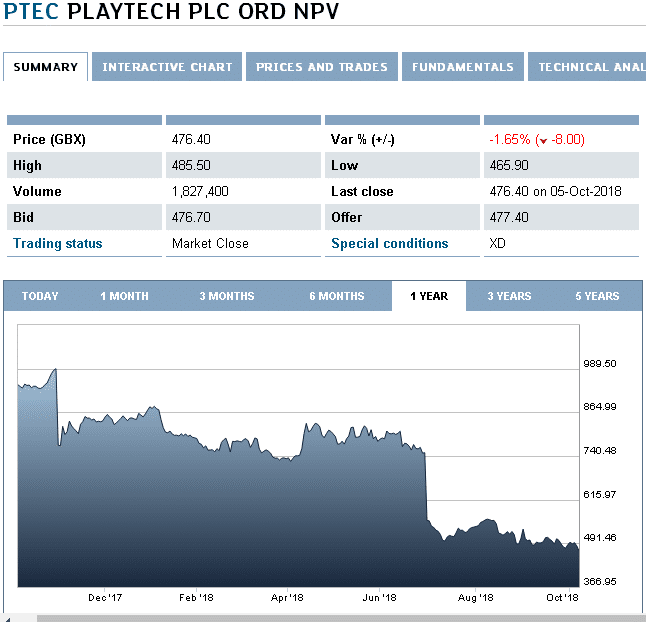

The best place to pick up the Playtech story is to review its share price chart for the past year and detail what may have caused the obvious “irregularities” that appear:

For those of you reading about Playtech for the first time, it’s reputation is as “the world’s largest online gaming software supplier traded on the London Stock Exchange Main Market.” In 2015, Playtech had plenty of cash in the bank and a market cap of $3.7 billion. Teddy Sagi was eager to expand his footprint in the industry via the M&A route. Regulators, however, disapproved of the Plus500 takeover, and the past three years have been a troublesome road. Current market cap is down to roughly $2.0 billion, and share price has dropped from a high of over 1,000 pence down to 476 at its latest close.

The last highpoint was August of 2017. Playtech had clawed its way forward after trimming back overhead and continuing to expand by acquiring companies, this time off shore where the FCA could not block its efforts. Around this time, Mr. Sagi decided to exit the Playtech scene and sold 36.5 million shares, thereby reducing his ownership from 17.8% down to 6.3% of his pride and joy. As we reported at that juncture: “He would move onto managing his real estate portfolio and private investments, which includes a jaunt into the blockchain technology arena. He remained Playtech’s largest stockholder, but he could no longer appoint directors.”

86% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

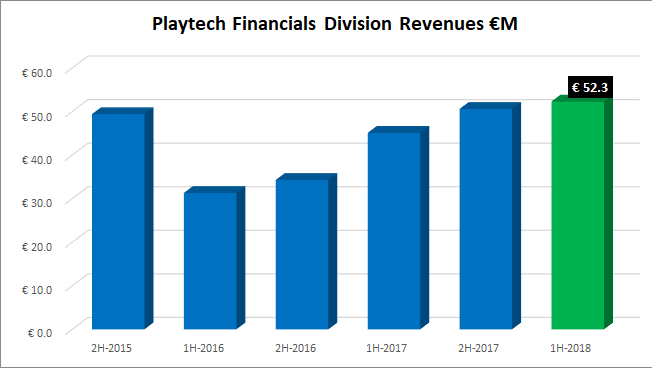

In the Post-Sagi days that followed, Playtech stumbled along, having to make not one but two earnings warnings, the kiss of death, when it comes to impressing investors. Shares promptly lost another third of their value. Despite a few bumps along the way, Playtech’s newly created Financial Division was busy delivering increasing year-over-year revenue growth from 2016 onward. These revenues, however, account for something just north of 12% of total revenues. The problems were with the core business and concentrated in Asia, based on management comments to shareholders.

In a recent communiqué, the news was downbeat: “Average daily revenue in Asia continues to be impacted by an increasingly competitive backdrop. Towards the end of the first half, this market has seen a particularly aggressive pricing environment from new entrants to the market and this has impacted revenue. The management team continues to take steps to protect Playtech’s position in the region and to drive revenue generation. However, given the recent decline and in the absence of any change in market dynamics, the Group expects a significant impact on revenue throughout the rest of the year.” Earnings warnings are never any fun, since a share bashing is the result.

When first-half performance figures were released in August, a small, but short rally was the upshot. Except for a reclassification of the timing of a €29 million write-down of expenses between fiscal halves, the figures were not really that bad. Yes, revenues only grew by 4%, a reflection of the ongoing pushback in Asia, but see for yourself:

What about the remainder of 2018? Here is more clarification: “Looking to the remainder of the year, the current run rate in Asia is materially below both the average in H2 2017 and the average, which was expected for H2 2018 at the start of the year. If the current run rate in Asia continues unchanged for the remainder of 2018, including no material improvement in Malaysia, Playtech’s expected revenue from Asia will be c. €70 million lower than original expectations.” Gulp! Now we are talking about material losses.

86% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Mor Weizer, the CEO at the helm, conceded: “Clearly the recent trading performance in

Asia is disappointing. We have taken steps to further support our partners in the region and we will continue to work to preserve our position in the face of an increasingly competitive environment”. To his and the management team’s credit, there were additional messages that initiatives in other regions are prospering, as in Europe, and potentially a big win for the firm, as “regulatory developments in the US represent a significant opportunity for the Group”. With respect to new ESMA regulations over CFDs, the company has “decided to take a prudent approach to marketing spend on new customer acquisition”, a nice way of saying that retaining customers may be difficult.

The market is not that impressed. In recent months, management has gone about the job of cleaning up the balance sheet related to various M&A activities. These actions are yielding net gains that will be recognized in the remainder of 2018. Do you remember the Plus500 takeover debacle? Investments from way back when were finally liquidated for a hefty profit: “On September 7th, Playtech said it had sold its entire holding of approximately 11.4 million ordinary shares in Plus500 at a price of 1,550 pence per ordinary share. Thus, Playtech realized gross proceeds of approximately £176 million (equivalent to approximately €196 million at the time the announcement was made)”.

Where is this new source of cash flow going? Playtech says, “It will use the proceeds for general corporate purposes and debt reduction.” The firm has also remained on the acquisition trail, and part of the cleanup will necessarily involve refinancing related liabilities on the balance sheet. In that regard, Playtech announced: “The successful pricing of €530 million 3.75 % senior secured notes due 2023.”

Actions like these may not grab the headlines of the day or cause a spike in the market, but institutional hedge funds do find favor with these types of actions on behalf of the respective management team. There have been positive developments on this front. Odey Asset Management, a long-time investor in rival Plus500, has purchased a 5% share in Playtech, as well, literally a hedge from a hedge fund manager. Setanta Asset Management, an Ireland-based value investor, has bought a 3% share in the firm. This fund is actually owned by a Canadian group. What do these hedge funds see?

86% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

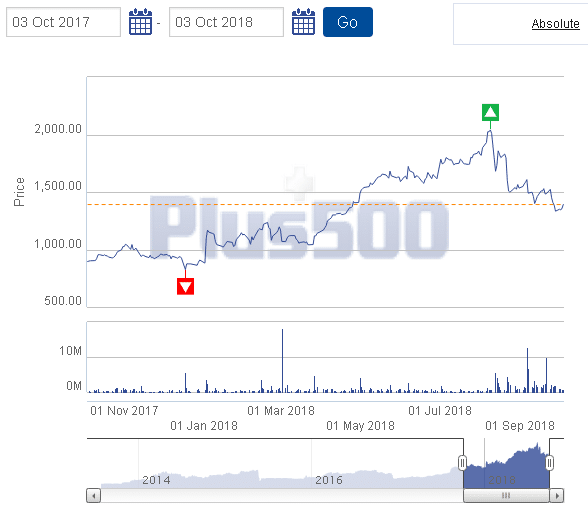

While Playtech floundered, Plus500 took off for the races.

One would think that two similar entities in the same industry would face similar obstacles on the way to prosperity or peril, but when one compares the histories over the last three years for both Playtech and Plus500, one comes away dumbstruck by how the fates of these two enterprises could be so diametrically different. Once freed from the clutches of the takeover bid from Playtech, Plus500 has soared.

If you scroll back a few paragraphs, you will remember that, in 2015, Playtech, then with a market cap of $3.7 billion, had offered Plus500 a whopping offer of $702 million, a figure I failed to mention above. Fast forward three years, and what do we find? Playtech has a market cap of $2.0 billion, while Plus500 stands at $1.9 billion. How is that for a tale of two companies?

86% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

It would be understandable if there were a great deal of angst on the Playtech board about this matter. Was there ever a chance to persuade regulators to accept the original proposal, if a few modifications had been made? Surely there were discussions, but most everyone has been close lipped on the matter. Regulators are not always amenable to reversing their decisions. One can always speculate as to whether Plus500 management would have had the freedom to fly as they have, but Mr. Sagi had certainly picked out a bargain, no doubt on that score. A bigger question is why did not the industry leader, the IG Group, swoop in like a “White Knight” and grab up Plus500 at bargain basement prices? IG’s market cap today stands at a paltry $3.1 billion in comparison. I would suspect that their shareholders and board are a bit angry, as well.

This price chart says it all. The dip came after “Plus500 reported second quarter results, which were strong, but not nearly as spectacular as a record-setting Q1” and in anticipation of CFD changes in Europe, instituted by ESMA. Founders of the firm quickly and gleefully unloaded shares worth £145 million, but two hedge funds, Blackrock in the U.S. and Axxion in Luxembourg, promptly secured 7% and 3% stakes, respectively. Does this storyline sound eerily familiar?

86% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money.

Concluding Remarks

Gambling enterprises are extremely profitable, even when regulators attempt to protect the interests of the general public. In this venue, the rich get richer, and the poor get richer, too.

Related Articles

- Forex vs Crypto: What’s Better For Beginner Traders?

- Three Great Technical Analysis Tools for Forex Trading

- What Does Binance Being Kicked Out of Belgium Mean for Crypto Prices?

- Crypto Traders and Coin Prices Face New Challenge as Binance Gives up its FCA Licence

- Interpol Declares Investment Scams “Serious and Imminent Threat”

- Annual UK Fraud Audit Reveals Scam Hot-Spots

Forex vs Crypto: What’s Better For Beginner Traders?

Three Great Technical Analysis Tools for Forex Trading

Safest Forex Brokers 2025

| Broker | Info | Best In | Customer Satisfaction Score | ||

|---|---|---|---|---|---|

| #1 |

|

Global Forex Broker |

BEST SPREADS

Visit broker

|

|

|

| #2 |

|

Globally regulated broker |

BEST CUSTOMER SUPPORT

Visit broker

|

|

|

| #3 |

|

Global CFD Provider |

Best Trading App

Visit broker

|

|

|

| #4 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #5 |

|

Global Forex Broker |

Low minimum deposit

Visit broker

|

|

|

| #6 |

|

CFD and Cryptocurrency Broker |

CFD and Cryptocurrency

Visit broker

|

|

|

|

|

|||||

Forex Fraud Certified Brokers

Stay up to date with the latest Forex scam alerts

Sign up to receive our up-to-date broker reviews, new fraud warnings and special offers direct to your inbox